KBRA Releases Research – Strong Retail Sales and Employment Gains in December Point to Continued Momentum Heading Into 2024

Retail sales increased by a solid 0.6% month-over-month (MoM) in December, according to a U.S. Department of

Commerce report released January 17, 2024. The increase was accompanied by an uptick in monthly nonfarm employment

growth, with both datapoints notching their strongest growth in three months in a sign of continuing resilience. In this

edition of KBRA’s monthly commentary on retail sales, we discuss these trends, the softening performance of state sales

tax receipts, and why the recent uptick in retail sales and employment momentum may not last through 2024.

Key Takeaways

▪ Retail sales in December notched their strongest MoM growth since September and were up by a solid 5.6% yearover-year (YoY).

▪ Rapid jobs growth through year-end supported retail sales performance in 2023 but slowing employment gains could

indicate more tepid spending this year.

▪ State sales tax collections are already slowing, with September through November collections trailing headline inflation

in nine of 11 states* tracked by KBRA (for which data is available).

▪ Sharply reduced personal savings and growing loan balances signal headwinds to retail sales growth in 2024, as does

the Federal Reserve’s December projection for the need for three rate cuts this year.

Recommended : Untraditional Ways To Discover Tech Talent And Promising Software Projects

Retail Sales Are Outpacing Inflation

Retail sales and inflation trended lower as the Fed tightened rates between March 2022 and July 2023. Retail sales have

subsequently gained momentum while inflation has stabilized slightly above 3% YoY. Retail sales lagged inflation through

much of the year but by December outpaced inflation by 2.3% YoY, reflecting a return to growing real consumption.

Retail Sales by Category

Retail sales growth accelerated to a strong 0.6% MoM in December, lifted by growth in nine of 13 categories. In contrast,

retail sales for the month were up by an also solid 5.6% YoY.

Auto sales, the largest category, were up 1.1% MoM and 10.3% YoY. Vehicle prices were similar YoY with new vehicle

prices up 0.4% and used vehicle prices down 1.3%. Strong sales reflect easing pent-up demand as production capacity

and inventories have recovered from pandemic-era supply chain disruptions. Online sales increased 1.5% MoM and

were up 9.7% YoY as consumers continued to shift an ever-growing portion of spending online.

In contrast, home improvement and furniture sales were up 0.4% and down 1% MoM, respectively, and were among the

weakest performers YoY. The 2.3% YoY decline in home improvement and 4.7% YoY decline in furniture sales were likely

partly due to a combination of diminished pandemic-era excess savings and the significant slowdown in home sales since

the Fed started hiking rates. Gasoline station sales were down 1.3% MoM and 6.6% YoY, with the change over both periods

corresponding closely with movement in gasoline prices. The average retail price for a gallon of gasoline was $3.058 in the

week ended January 15, up less than 0.1% from four weeks prior.

Employment Growth Remains Strong

Employment growth has slowed significantly over the last two years but has remained relatively resilient through the rate

tightening cycle, which has been supportive of retail sales strength. KBRA commented earlier this month on the outsized

role of government jobs in employment growth last year and the 216,000 jobs added MoM in December, with total jobs

growth remaining well above the average monthly gain of 141,000 in the decade of growth preceding the pandemic

(see Government Hiring Pads Strong but Slowing U.S. Employment Gains).

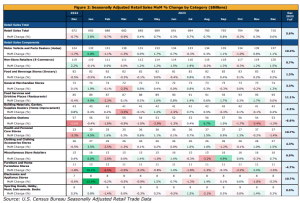

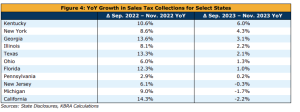

State Sales Tax Collections Remain Slow

State sales tax collections in September through November 2023 trailed inflation of 3.4% YoY in nine of 11

* states tracked

by KBRA. State receipts, which account for more than three-quarters of total general sales taxes in the U.S., declined in

three of the 11 states, led by California with receipts down 2.2% YoY. Deteriorating performance relative to stimulusfueled gains observed in 2022 point to a softening economic environment in much of the country.

What’s Next?

Strong retail sales and jobs growth in December point to a resilient economy crossing into the new year, but there are signs that this momentum may not last. The personal savings rate trended sharply lower in 2H 2023 and consumer loans were up nearly 10% YoY in December, signaling that household budgets may already be stretched. Further, in its December quarterly summary of economic projections, the Fed forecast the need for three rate cuts this year, implying an expectation that the long and variable lagged effects of short-term rates maintained at the present level will slow economic growth in 2024. Geopolitical risks to economic growth also continue to rise. Conflict in the Middle East is disrupting international trade through the Red Sea and a prolonged conflict resulting in a broad and sustained rerouting and delay of shipping activity in the region could exert upward pressure on prices in the U.S., complicating the Fed’s efforts to stabilize prices while avoiding a recession. KBRA will monitor these and other developments with an eye toward their implications for retail sales performance and sales tax collections.

Latest HRtech Interview Insights : HRTech Interview With Tommy Barav, Founder And CEO At TimeOS

[To share your insights with us, please write to pghosh@itechseries.com ]